“Industrial Machine Vision Market Forecast in the US: Opportunities and Challenges”

The United States Industrial Machine Vision Market is characterized by strong competition and rapid innovation, driven by increasing industrial demand for automated inspection and smart manufacturing solutions. The market includes a mix of global machine vision leaders, specialized U.S.-based technology providers, camera manufacturers, sensor developers, and software companies offering advanced vision analytics. Competition is largely shaped by product innovation, system integration capabilities, customer support services, and the ability to deliver flexible solutions for diverse industries.

Major market participants focus heavily on research and development to enhance camera performance, sensor capabilities, and software intelligence. Machine vision is an evolving field, and companies that can deliver high-speed inspection solutions with improved accuracy gain a significant advantage. Manufacturers increasingly demand vision systems capable of handling complex inspection tasks, such as surface defect detection, 3D measurement, robotic guidance, and automated quality control. As a result, vendors continuously improve their product offerings by incorporating AI-driven algorithms, deep learning-based defect recognition, and advanced imaging technologies.

The competitive environment is also shaped by the growing demand for turnkey machine vision solutions. Many manufacturers lack the internal expertise required to design and implement complex vision systems. This has led to rising demand for complete machine vision packages that include cameras, lighting, sensors, software, and integration services. Vendors that provide full-service solutions, including installation, calibration, training, and long-term support, are gaining market share. System integrators also play a major role, acting as a bridge between machine vision technology providers and industrial customers.

Software has become one of the most important differentiators in the market. Traditional machine vision systems relied on rule-based programming, which required extensive configuration and was less adaptable to changing product designs. Modern vendors now focus on offering intelligent vision software platforms that simplify configuration through graphical user interfaces and AI-based learning models. Deep learning vision software has become particularly important for industries dealing with highly variable products, such as consumer goods manufacturing and packaging. Vendors offering strong software ecosystems often secure long-term partnerships with manufacturers.

Strategic partnerships and acquisitions have also become common in the market. Companies frequently collaborate with robotics manufacturers, automation providers, and industrial IoT solution developers to deliver integrated smart factory solutions. Partnerships help machine vision companies expand their reach into new industrial sectors and improve system compatibility with automation platforms. In addition, acquisitions allow large companies to strengthen their portfolios by adding new technologies, such as 3D imaging, hyperspectral sensors, or edge AI processing tools.

Another major competitive factor is the ability to deliver scalable solutions. Large manufacturing plants may require hundreds of cameras and inspection points across multiple production lines. Vendors that provide scalable architecture, easy software upgrades, and centralized monitoring systems are more attractive to high-volume industries. Scalability is also critical for logistics and warehouse automation, where machine vision is used for package tracking, barcode scanning, and sorting operations. Companies that provide modular and scalable systems can expand with customer needs.

Pricing and cost-effectiveness remain important competitive elements. While machine vision systems offer strong ROI, high initial investment can still be a barrier for small and medium-sized enterprises. Vendors are increasingly developing affordable systems and cloud-based subscription models that lower upfront costs. Additionally, improvements in camera manufacturing and computing hardware have helped reduce system prices over time. This has expanded market adoption beyond large industrial enterprises to smaller manufacturers seeking automation benefits.

Customer support and after-sales services also play a key role in vendor competitiveness. Machine vision systems require regular calibration, software updates, and troubleshooting. Vendors that offer strong customer support, remote monitoring, and predictive maintenance features gain a competitive edge. Many companies now provide online training programs and digital support tools to help customers maximize system performance.

Категории

Больше

This year marks an exciting evolution in mobile gaming, especially for fans of Netflix's popular series and WWE enthusiasts. Expect to see a surge in titles that blend intense action, compelling storytelling, and player agency, offering a richer gaming experience. Netflix has become the exclusive platform for some of the most adrenaline-pumping WWE mobile games, including the highly anticipated...

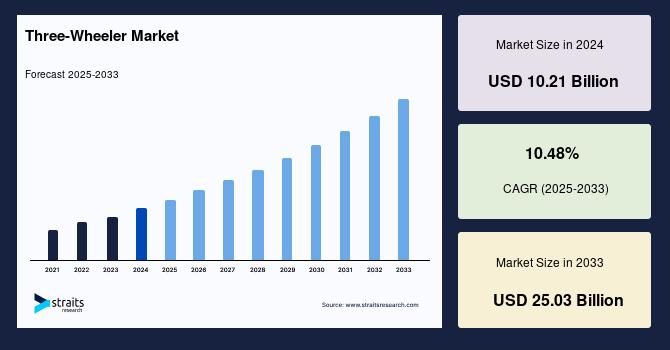

Three-Wheeler Industry Outlook: Straits Research has introduced a detailed analytical study on the Three-Wheeler Market, offering insights into market valuation, segmentation framework, and long-term growth trajectory. The publication delivers a structured overview of market drivers, constraints, technological advancements, and strategic developments shaping the industry. In addition, it...

Starkes Pokémon-Team Steigere deine Erfolgschancen im Pokémon TCG Pocket mit einem kraftvollen Elezard- und Magnezone-Deck. Dieses aggressive Team setzt auf elektrische Stärke und hohe Schadenspunkte, um deine Gegner zu dominieren. In der neuesten Erweiterung Feuerrote Flammen tritt der Arenaleiter Citro mit einem Team aus Elektro-Pokémon an, das speziell auf schnelle...

Global Streaming Giant Secures Rights to Korean Nuclear Disaster Film Netflix has expanded its international content library by acquiring streaming rights to the South Korean disaster thriller "Pandora" in a deal with Next Entertainment World. The announcement came from Singapore on November 8, 2016. The nuclear disaster blockbuster, directed by Park Jung-woo (previously known for "Deranged"),...

Season 2 Espionage Thrills Noah Centineo Returns as CIA Lawyer in Action-Packed Second Season The highly anticipated second season of the espionage thriller has finally arrived on streaming platforms, bringing viewers back into the chaotic world of Owen Hendricks, portrayed by Noah Centineo. This season raises the stakes significantly as the young CIA attorney faces an array of new threats....