An Overview of the Mature and Evolving France Remittance Industry

The France Remittance industry stands as one of Europe's largest and most established markets for cross-border personal money transfers, deeply rooted in the country's long history of immigration and its strong economic and cultural ties to nations across Africa, the Middle East, and other parts of Europe. This mature industry is primarily characterized by significant remittance outflows, driven by a large and diverse immigrant population sending money back to support families in their home countries. The primary remittance corridors from France lead to the Maghreb region (Morocco, Algeria, Tunisia), Sub-Saharan Africa (particularly Senegal, Mali, and Côte d'Ivoire), and other European countries like Portugal and Romania. The industry is a highly competitive and sophisticated ecosystem, featuring a triad of dominant players: traditional banks, global Money Transfer Operators (MTOs), and a rapidly growing segment of digital-first fintech companies. The entire market operates under the stringent regulatory framework of the European Union, which prioritizes consumer protection, anti-money laundering (AML), and transparency, shaping the competitive dynamics and operational requirements for all service providers.

The traditional foundation of the French remittance industry has long been composed of high-street banks and global MTOs like Western Union and MoneyGram. For decades, banks have facilitated international transfers for their account-holding customers, though often through the slow and expensive SWIFT network, making it a less preferred channel for smaller, frequent remittances. The true incumbents in the mass-market remittance space have been the MTOs. These companies have built vast and formidable networks of physical agent locations, often situated in post offices, convenience stores, and dedicated storefronts in neighborhoods with large immigrant populations. Their primary value proposition has been accessibility and trust, offering a straightforward, over-the-counter cash-to-cash service that is essential for senders who may be less comfortable with digital technology and for recipients in countries with low banking penetration. This physical presence remains a significant asset, and the "peace of mind" associated with a well-known brand continues to anchor their strong position in the market, especially among older demographics.

The most significant and disruptive force in the industry today is the rapid proliferation of digital and mobile-first remittance platforms. A new generation of fintech companies, both European and global, is fundamentally challenging the old guard by offering a purely digital, app-based alternative. Players like Wise (formerly TransferWise), Remitly, WorldRemit, and Sendwave have gained significant market share by offering a compelling value proposition centered on lower costs, better exchange rates, greater speed, and superior convenience. These platforms allow users to send money from their bank account or debit card directly to a recipient's bank account, mobile money wallet, or for cash pickup, all from their smartphone. By leveraging more efficient payment rails and operating with a lower overhead than their brick-and-mortar competitors, they can pass significant savings on to the consumer. This digital-first model has resonated powerfully with younger, more tech-savvy generations of migrants and has forced the entire industry to innovate, driving down prices and improving service levels across the board.

The regulatory environment, governed by both French national law and overarching EU directives like the Payment Services Directive (PSD2), plays a crucial role in shaping the industry's structure and operations. These regulations impose strict requirements on all remittance providers regarding customer due diligence (Know Your Customer - KYC), anti-money laundering (AML) checks, and combating the financing of terrorism (CFT). This creates a high barrier to entry and requires significant ongoing investment in compliance technology and personnel. Furthermore, regulations promoting transparency require providers to clearly disclose all fees and the exchange rate used before a transaction is made, which has helped to empower consumers and increase price competition. The advent of Open Banking under PSD2 is also beginning to impact the industry, allowing licensed third-party providers to initiate payments directly from a user's bank account (with their consent), which can further streamline the digital remittance process and foster greater innovation and competition among service providers.

Explore More Like This in Our Regional Reports:

الأقسام

إقرأ المزيد

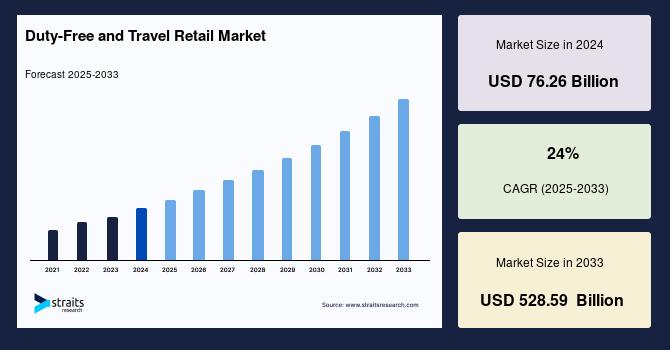

Duty-Free and Travel Retail Market Growth, Global Tourism Shopping Trends and Forecast to 2033 Duty-Free and Travel Retail Industry Outlook: Straits Research has introduced a detailed analytical study on the Duty-Free and Travel Retail Market, offering insights into market valuation, segmentation framework, and long-term growth trajectory. The publication delivers a structured...

The digital world runs on a foundation of powerful servers, but these servers generate an immense amount of heat, giving rise to the critical and highly specialized Data Center Cooling industry. The core mission of this essential sector is to manage the thermal environment of the data center, ensuring that the vast arrays of IT equipment—servers, storage, and networking...

A decentralized messaging network is experiencing a significant uptick in registrations, coinciding with user concerns over a major platform's upcoming mandatory verification policies. This shift highlights a growing search for communication tools that prioritize user sovereignty and data control, though the landscape of digital regulation presents universal challenges. The appeal lies in the...

In a groundbreaking move, Netflix announced the upcoming release of a compelling new biographical series centered around a shocking real-life encounter. Titled "The Day I Met El Chapo: The Kate del Castillo Story," this three-part documentary will premiere exclusively on the streaming platform on October 20, 2017. This series offers an intimate glimpse into the life of renowned Mexican actress...

Netflix is charting a new course into the world of comics, but this move is about more than just ink on paper. The streaming giant's acquisition of Millarworld is a strategic play, focused on cultivating original stories from the ground up. Mark Millar, known for translating comics to blockbuster films, will now develop and test narratives with dedicated fans first. Successful stories will...