The Future of Risk Management in the Business Insurance Market 2025–2035

The rapid adoption of enterprise technology across global industries has completely altered the corporate risk landscape, sparking a new wave of demand for advanced protection products. Traditional commercial coverage portfolios were designed primarily for physical assets like factories, warehouses, and tangible inventory. However, the modern corporate footprint is increasingly defined by digital assets, cloud infrastructure, proprietary algorithms, and massive databases of sensitive consumer information. This shift from physical to digital operations exposes businesses to distinct vulnerabilities, including systemic ransomware attacks, catastrophic data breaches, operational downtime from software outages, and complex intellectual property disputes. Consequently, standard commercial liability policies are no longer sufficient, driving an urgent need for specialized, tech-focused coverage options that address the unique realities of the modern digital economy.

This structural shift toward digital-first business models is a primary engine behind the steady expansion of the commercial protection industry. Analyzing the broader patterns of this development through a reliable Business Insurance Market growth framework reveals how rapidly carriers are shifting their resources to address modern technology risks. Underwriters are investing heavily in advanced data analytics, artificial intelligence tools, and real-time risk monitoring systems to better evaluate and price these complex, intangible exposures. For technology buyers and corporate risk managers, this evolution highlights the importance of working closely with brokers who understand tech-driven liabilities. By monitoring these industry expansion metrics, companies can see how new protection products are developed, allowing them to secure cutting-edge coverage for emerging risks like artificial intelligence liabilities, algorithmic errors, and cloud-vendor vulnerabilities.

Frequently Asked Questions

-

Why are traditional commercial property insurance policies insufficient for digital-first enterprises? Traditional property policies generally cover tangible, physical damage to real assets, meaning they do not provide protection for intangible losses like data corruption, digital asset theft, or lost revenue from cyber extortion.

-

What role does artificial intelligence play in how modern underwriters evaluate commercial technology risks? Underwriters use artificial intelligence to scan vast amounts of historical claims data, evaluate a company's cyber security posture in real time, and build more accurate, predictive risk profiles for pricing policies.

➤➤➤Explore MRFR’s Related Ongoing Coverage In Semiconductor Industry:

Solid State Power Amplifier Market

Storage Refrigeration Monitoring Market

Kategorien

Mehr lesen

Sony's grip on its digital infrastructure appeared to weaken dramatically as fresh security breaches emerged midweek, pushing the total count of confirmed intrusions to double digits. Beyond the massive PlayStation Network compromise that forced a shutdown lasting more than 20 days, these additional violations suggest the company's protective measures may be fundamentally inadequate. Three...

A decentralized messaging network is experiencing a significant uptick in registrations, coinciding with user concerns over a major platform's upcoming mandatory verification policies. This shift highlights a growing search for communication tools that prioritize user sovereignty and data control, though the landscape of digital regulation presents universal challenges. The appeal lies in the...

A landmark legal decision in Paris has mandated five prominent VPN providers to restrict access to a series of illegal football streaming platforms, marking a significant step in the ongoing battle against online piracy. The order, issued on December 18th, directs NordVPN, Surfshark, Proton VPN, ExpressVPN, and CyberGhost to block access to 13 specific piracy sites, aligning with the interests...

Команда PUBG: BATTLEGROUNDS с радостью поздравляет своих игроков с наступлением 2026 года и подготовила для них праздничный сюрприз — возвращение Весеннего феста 2025. В рамках этого события в игру вновь добавлены уникальные скины оружия, а также новые цветовые схемы и специальные предложения, предназначенные для всех участников. Особое внимание уделено обновленным улучшаемым скинам из...

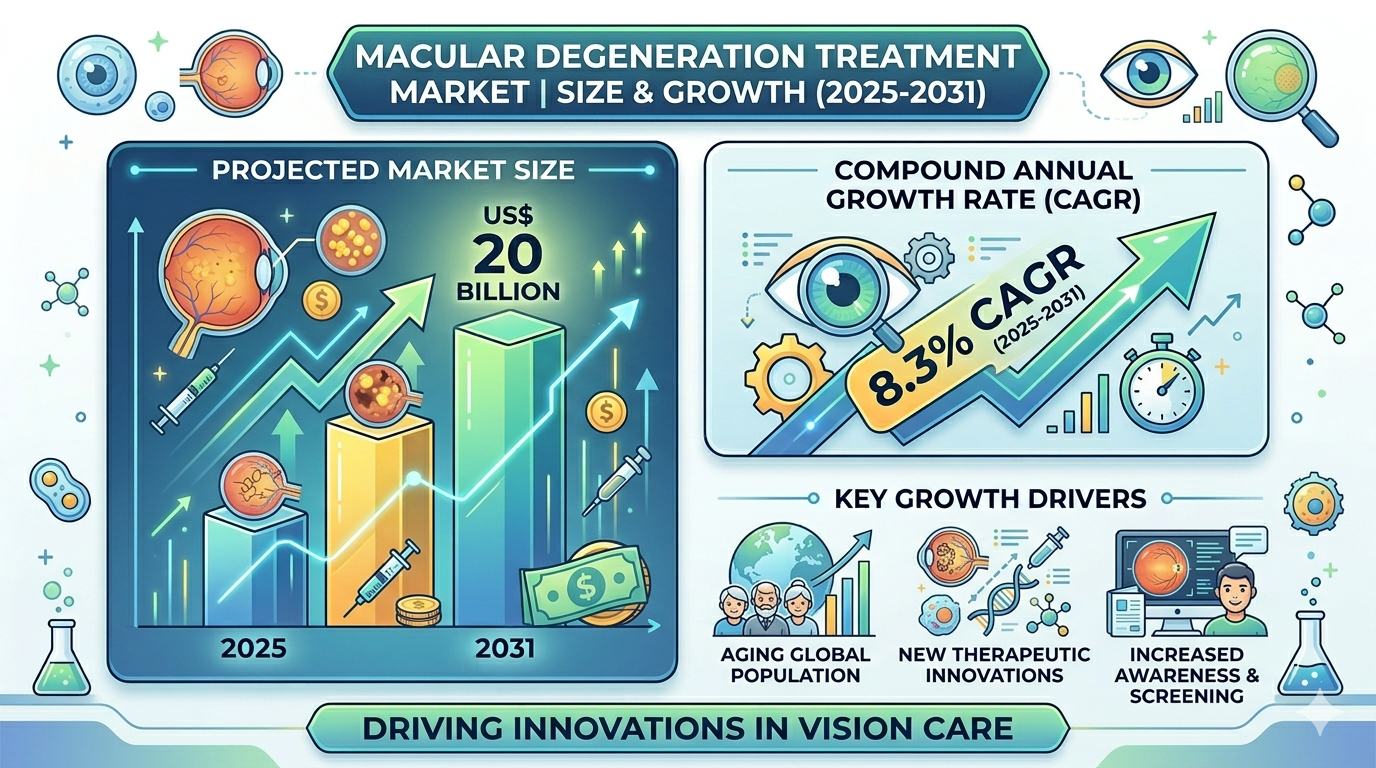

Macular degeneration is a progressive retinal condition that leads to deterioration of central vision, significantly impacting daily activities such as reading and driving. It is widely prevalent among the elderly population and is considered one of the primary causes of vision loss globally. Rising Prevalence of Age-Related Vision DisordersThe growing aging population worldwide is a key...