How Industry Trends Demand Surges

The competitive landscape of the India OTT market is undergoing significant transformation, fueled by evolving consumer preferences and technological advancements. As traditional media channels face increasing competition from digital platforms, the market is experiencing a profound shift towards on-demand content consumption. With a projected market size of USD 19,250 million by 2035, the industry is set to witness a remarkable CAGR of 17.20%. The continuous influx of new entrants and existing players adapting their strategies to meet consumer demands exemplifies the dynamic nature of this market. According to Market Research Future, the market is expected to reach USD 3,900 million in 2024 and USD 4,509.18 million in 2025, indicating a robust growth trajectory that attracts considerable investment and innovation.

Key industry participants such as Netflix (US), Amazon Prime Video (US), and Disney+ (US) are leading the charge in this competitive environment, each vying for a greater share of the burgeoning OTT market. These platforms have significantly expanded their content libraries, incorporating both international and local programming to cater to diverse viewer preferences. In addition to established names, regional players like Sony Liv (IN) are carving out their niche by focusing on localized content that resonates with Indian audiences. The rising popularity of ad-supported models, which allow for alternative revenue generation, is further diversifying the offerings available to consumers. This competitive landscape also reveals a focus on technological enhancements, with advancements in streaming quality and user experience playing a critical role in maintaining viewer engagement.

Several key factors influence the competitive dynamics within the India OTT market. First, the increasing availability of affordable high-speed internet enables consumers from various backgrounds to access streaming services, paving the way for market expansion. The preference for binge-watching and the demand for diverse content are driving platforms to innovate continuously. Furthermore, the pandemic has had a lasting impact on consumer behavior, with many individuals now prioritizing digital entertainment over traditional viewing options. This behavioral shift is compelling companies to adapt their service offerings to accommodate changing viewer expectations. Additionally, the rise of mobile viewership, enabled by affordable data plans, is reshaping how content is consumed, further intensifying competition among providers The development of industry trends continues to influence strategic direction within the sector.

Geographically, India’s OTT market showcases unique consumption patterns influenced by regional preferences. Major cities like Mumbai and Bangalore are leaning towards premium content from international platforms such as Hulu (US) and HBO Max (US), while smaller cities are embracing localized content from platforms like iQIYI (CN) and Tencent Video (CN). This regional analysis indicates that the strategies employed by OTT providers must reflect the cultural nuances of their target audiences. As a result, companies must not only invest in high-quality content but also enhance their distribution strategies to effectively reach viewers across different regions of India.

The evolving landscape presents numerous investment opportunities within the India OTT Market, particularly in content creation and technological advancements. As platforms strive to differentiate themselves, there is a growing need for innovative programming that captures diverse cultural narratives. Additionally, the adoption of hybrid monetization models that blend subscription and ad-supported services is becoming increasingly relevant. Investing in advanced analytics and machine learning technologies can empower platforms to enhance user experiences and optimize content recommendations. The market dynamics suggest that companies prioritizing customer engagement and personalized content delivery will likely experience sustained growth.

Analytically, the surge in OTT subscriptions has been remarkable, with approximately 40% of Indian households reported to have at least one OTT subscription as of 2023, a significant increase from just 20% in 2019. This rise correlates strongly with the availability of affordable smartphones and data plans, which have led to a 25% increase in mobile video consumption year-on-year. Real-world examples such as the success of local content series like "Paatal Lok" on Amazon Prime Video demonstrate the effectiveness of tailored content strategies, where localized storytelling has been pivotal in attracting a wider audience. Moreover, the implementation of targeted advertising, with an expected growth of 30% in ad revenues for OTT platforms by 2025, indicates that companies that leverage data analytics to understand viewer behavior will not only enhance user engagement but also drive significant revenue growth.

As the industry moves forward, the future outlook of the India OTT market appears promising. Projections indicate that by 2035, the market will continue to thrive, supported by ongoing innovations in content and technology. The integration of AI and data analytics will be pivotal in shaping viewer experiences and personalizing content delivery. Future advancements, such as interactive content and live streaming, are expected to capture consumer interest and loyalty. As competition intensifies, companies will need to develop agile strategies to capitalize on emerging trends and maintain relevance in the dynamic marketplace.

|

Us Multi Modal Generation Market |

|

China Passive Authentication Market |

|

Europe Passive Authentication Market |

|

Japan Passive Authentication Market |

|

South America Passive Authentication Market |

|

China Web Analytics Market |

Categorias

Leia mais

Introduction About Michael Olise Born on December 12, 2001, in London, Michael Olise is a talented French professional footballer recognized for his exceptional skills and versatility on the right side of midfield. Having begun his journey at Reading’s youth academy at just 15 years old, Olise rapidly progressed, breaking into the first team two years later and demonstrating remarkable...

Top Comedy Selections A good laugh can be a perfect remedy after a demanding day, whether you're at work or school. Netflix provides an extensive array of comedy specials and films to lift your spirits. We've curated a list of top-notch comedies currently streaming, spanning various styles such as stand-up routines, romantic comedies, horror-infused humor, and satirical hits. Prepare yourself...

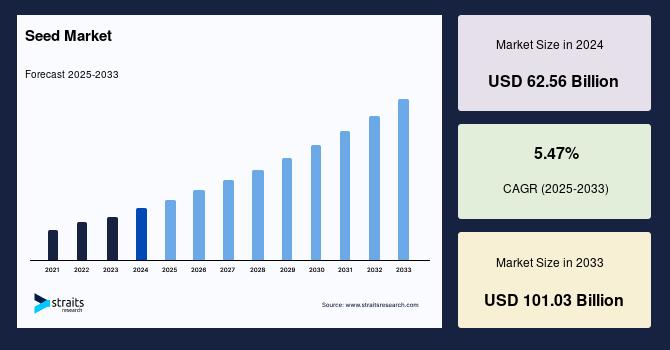

Seed Market Overview A new report titled “Global Seed Market Professional Report 2025-2033” has been added by Straits Research to its repository of research reports. The report analyzes and estimates the market on a global, regional, and country level. The report offers data from previous years along with an in-depth analysis from 2025 to 2033 on the basis of revenue (USD Billion or...

The notion of an 'Internet health' body is being floated, prompting a debate over how to safeguard the digital ecosystem. Microsoft's Scott Charney, in a recent RSA Conference address, raised the possibility of a global cybersecurity entity, akin to public health organizations. He argued that just as public health measures protect communities, similar principles might apply to cyberspace....

Fairdeal is an online gaming and betting site that is growing quickly. It is made for people who want a smooth and safe experience when playing sports and casino games. Users can quickly get their online cricket ID and start looking at a lot of different betting markets by signing up easily. The platform is easy to use, which makes it great for both new and experienced players.You can bet...